Rate Cuts Have Arrived

Download the 9.20.24 Dynamic Market Update Presentation for advisors’ use with clients

By Kostya Etus, CFA®, Chief Investment Officer, Dynamic Investment Management

Last week—the week ending Sept. 13—was the best week of the year for the market, with the S&P 500 up over 4%. This puts the market up over 19% for the year, close to bull market territory. The bond market has also been performing well as interest rates have come down in anticipation of rate cuts, with the Bloomberg Aggregate up close to 5% on the year. Even real estate has rebounded with over a 14% return on the MSCI US Real Estate index. One of the reasons for these strong returns is that this entire year has led up to a momentous event—the first interest rate cut from the Federal Reserve (Fed) since March of 2020.

Below are the key economic data leading up to the Fed meeting and key outcomes from the meeting itself:

- Positive Economic Data: Leading up to the Fed meeting, we received three pieces of great news for the economy. Retail sales, industrial production and housing starts stood out in two ways in that they were all positive and beat expectations. These are all signs of economic strength and support a resilient consumer, manufacturing stability and perhaps a turnaround in the housing market.

- A Surprise Double Cut: The Fed was widely expected to make a single 0.25% cut in the interest rate, but they surprised with two, lowering by 0.50%, from 5.50% to 5.00%. Fed chair Jerome Powell emphasized that the larger cut is not due to expectations of an economic downturn, but instead a “recalibration” of central bank policy to achieve price stability without a painful increase in unemployment.

- Positive Economic Outlook: The Fed also released new economic forecasts and updated interest rate projections. They are expecting two more 0.25% cuts this year—perhaps in November and December—a full 1.00% cut next year, and another 0.50% in 2026, which if achieved, would end with rates at 3%. Additionally, inflation and GDP growth are expected to stay close to 2%, near target levels and long-term averages. Lastly, unemployment is expected to be 4.4%, which is below the historic average of about 5.7%.

Now that we have had the first rate cut as well as more defined expectations of future cuts and economic activity, we may have a better viewpoint from which to consider the outlook for the market. Lower rates are generally a tailwind for stocks, bonds and real estate. Companies can borrow more to grow businesses, bond prices increase, and real estate becomes more affordable. We have seen this play out this year in anticipation of the first cut, and we may have more to come as more cuts are on the horizon.

Good News for Markets

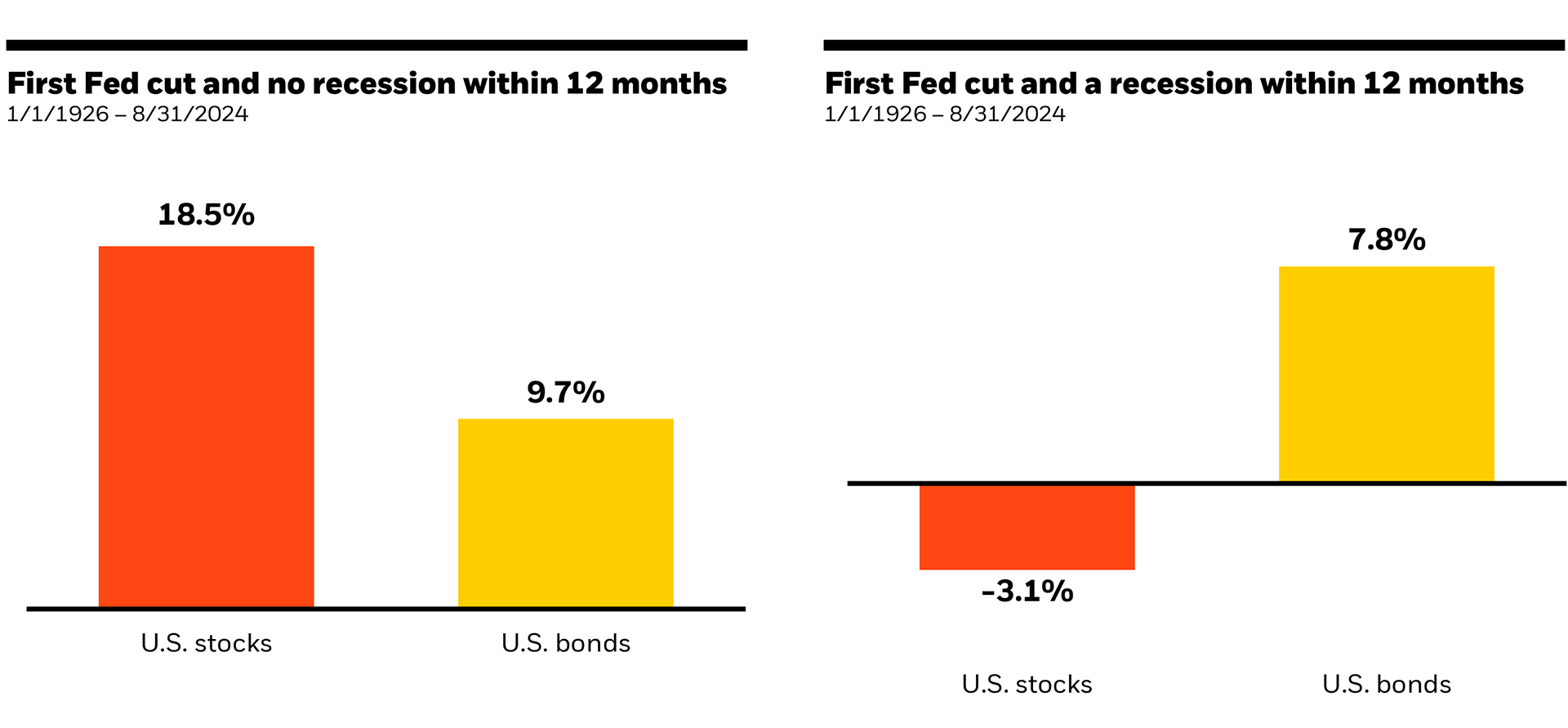

As mentioned above, Fed cuts may be good for the markets. That said, there have been times in the past when the Fed is lowering rates in anticipation of a recession, such as the situation during the Global Financial Crisis of 2008. Given recent economic data, as well as expectations from the Fed, a severe economic downturn is unlikely. Nonetheless, it is important to always be prepared, which is why we build diversified portfolios. So, what has history told us about stock and bond returns after the first Fed cut, both with and without a recession? The chart below helps answer these questions:

- Good for Stocks: If there is no recession, one year after the first Fed cut, U.S. stocks are up 18.5% on average. This is well above average annual returns for the stock market. Interestingly, even if there is a recession, the average drop is just over 3% for stocks. This reinforces the notion of just how valuable lower interest rates are for company growth.

- Good for Bonds: Bond returns have generally been positive over the long-term given their focus on income generation. That said their prices tend to go up when interest rates fall AND when there is market or economic turmoil, which is often seen in a recession. This is exhibited with the 8-10% returns after the first Fed rate cut, which is well above average annual returns for the bond market.

- Good for Diversified Portfolios: The most important part of the chart is that a combination of stocks and bonds is positive in both situations. We build diversified portfolios because the future is unpredictable and often expectations don’t play out how we may have planned. Diversified portfolios smooth out the investment ride and help investors be ready no matter what the markets or economy throws at them.

Stay diversified, my friends.

Stock and Bond Performance After a Rate Cut (With and Without a Recession)

Average Annual Returns 1926-2024

Source: Morningstar, Federal Reserve, NBER as of 8/31/24. U.S. stocks are represented by the S&P 500 TR Index from 3/4/57 to 8/31/24 and the IA SBBI U.S. Lrg Stock TR USD Index from 1/1/26 to 3/4/57. U.S. bonds are represented by the IA SBBI US Gov IT Index from 1/1/26 to 1/3/89 and the Bloomberg U.S. Agg Bond TR Index from 1/3/89 to 8/31/24. Past performance does not guarantee or indicate future results. Index performance is for illustrative purposes only. You cannot invest directly in the index.

As always, Dynamic recommends staying balanced, diversified and invested. Despite short-term market pullbacks, it’s more important than ever to focus on the long-term, improving the chances for investors to reach their goals.

Should you need help navigating client concerns, don’t hesitate to reach out to Dynamic’s Investment Management team at (877) 257-3840, ext. 4 or investmentmanagement@dynamicadvisorsolutions.com.

Disclosures

This commentary is provided for informational and educational purposes only. The information, analysis and opinions expressed herein reflect our judgment and opinions as of the date of writing and are subject to change at any time without notice. This is not intended to be used as a general guide to investing, or as a source of any specific recommendation, and it makes no implied or expressed recommendations concerning the manner in which clients’ accounts should or would be handled, as appropriate strategies depend on the client’s specific objectives.

This commentary is not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. Investors should not assume that investments in any security, asset class, sector, market, or strategy discussed herein will be profitable and no representations are made that clients will be able to achieve a certain level of performance, or avoid loss.

All investments carry a certain risk and there is no assurance that an investment will provide positive performance over any period of time. Information obtained from third party resources are believed to be reliable but not guaranteed as to its accuracy or reliability. These materials do not purport to contain all the relevant information that investors may wish to consider in making investment decisions and is not intended to be a substitute for exercising independent judgment. Any statements regarding future events constitute only subjective views or beliefs, are not guarantees or projections of performance, should not be relied on, are subject to change due to a variety of factors, including fluctuating market conditions, and involve inherent risks and uncertainties, both general and specific, many of which cannot be predicted or quantified and are beyond our control. Future results could differ materially and no assurance is given that these statements or assumptions are now or will prove to be accurate or complete in any way.

Past performance is not a guarantee or a reliable indicator of future results. Investing in the markets is subject to certain risks including market, interest rate, issuer, credit and inflation risk; investments may be worth more or less than the original cost when redeemed.

Investment advisory services are offered through Dynamic Advisor Solutions, LLC, dba Dynamic Wealth Advisors, an SEC registered investment advisor.

Photo: Adobe Stock