Download the Q1 2026 Dynamic Investing Insights for advisors’ use with clients

By Kostya Etus, CFA® Chief Investment Officer, Dynamic Asset Management

“Oh yes, the past can hurt. But from the way I see it, you can either run from it or learn from it.”

– Rafiki (Robert Guillaume), “The Lion King,” 1994

Market Review

We have gotten off to a rough start in the first quarter of 2026 with the global stock market down over 3%. Market weakness was primarily driven by geopolitical conflicts in the Middle East. Particularly, disruptions in energy markets caused oil prices to spike and inflation uncertainty took center stage. The Federal Reserve (Fed) effectively lowered expectations for interest rate cuts until the uncertainly abates, driving further volatility.

Not all areas of the market were equally impacted. There were wide dispersions among several asset classes and key market rotations emerged, including:

- Value outperformed growth by more than 8%.

- Small-cap stocks beat large-caps by more than 5%.

- International markets continued their momentum from last year, beating domestic stocks by over 3%.

- Real estate had a much needed rebound and was among the top performing asset classes, earning a positive return and beating global stocks by over 4%.

- Last, but not least, high-quality bonds did exactly what they were supposed to with roughly a flat return, outperforming global stocks by more 3%.

All told, it was a great quarter for diversified investors.

Looking beyond the headlines, we received several important economic datapoints which may help determine what to expect for the remainder of the year:

- Economy. The U.S. gross domestic product (GDP) growth, the primary measure of economic growth, had a relatively weak fourth quarter with an annualized growth rate of 0.5%. The weakness was attributable to sharp contractions in government spending and investment due to the government shutdown. That said, we finished 2025 with a full year growth rate of 2.1%. While lower than the 2.8% exhibited in 2024, it remains above the long-term average and target of about 2%. The economy still appears to be resilient and simply normalizing from previously high-growth levels.

- Inflation. The U.S. consumer price index (CPI) inflation rate jumped to 3.3% in March, primarily driven by higher energy costs due to the war with Iran. That said, the Core CPI rate, which excludes the more volatile food and energy prices, and the preferred measure by the Fed, came in at a more stable 2.6%. While this is slightly higher than the previous two months, the core inflation rate was below expectations, boding well for Fed rate cut expectations.

- Labor Market. The U.S. non-farm payrolls, a key measure of labor market health, showed an increase of 178,000 jobs in March after a revised contraction of -133,000 jobs in February. The whipsaw was caused by a strike in the healthcare sector, however, netting the two figures still results in a positive 45,000 jobs created. Perhaps more importantly, the unemployment rate fell to 4.3%, beating expectations. The labor market appears to be on stable footing, pointing to no recession on the horizon.

In summary, despite various economic disruptions, including a government shutdown, war in the Middle East and a strike in the healthcare sector, it seems that economic growth, inflation and the labor market are stable and in good health. This is good news for the stock and bond markets going forward, as well as for the potential of a maintained accommodative monetary policy from the Fed.

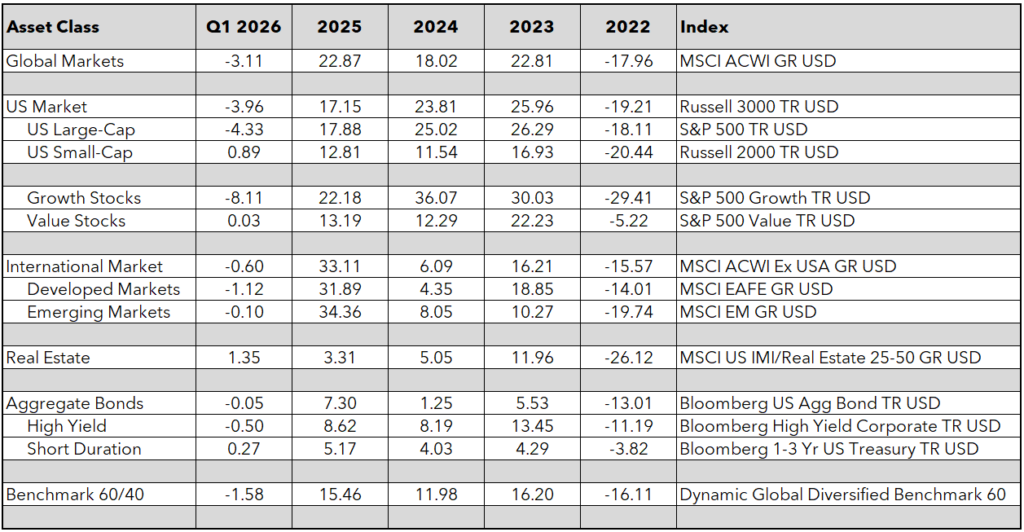

Asset Class Returns through Q1 2026

Source: Morningstar Direct as of March 31, 2026. Past performance does not guarantee or indicate future results. Dynamic Global Diversified Benchmark 60 consists of 45% Russell 3000 TR USD, 15% MSCI ACWI Ex USA GR USD, 40% Bloomberg Universal TR USD.

Top 3 Lessons:

- Intra-year market drops are common, but staying invested through the whole year often yields favorable results.

- While there are always reasons not to invest, ignoring the noise often rewards investors.

- During volatile and uncertain times, diversification is the safety seat belt that can keep investors calm.

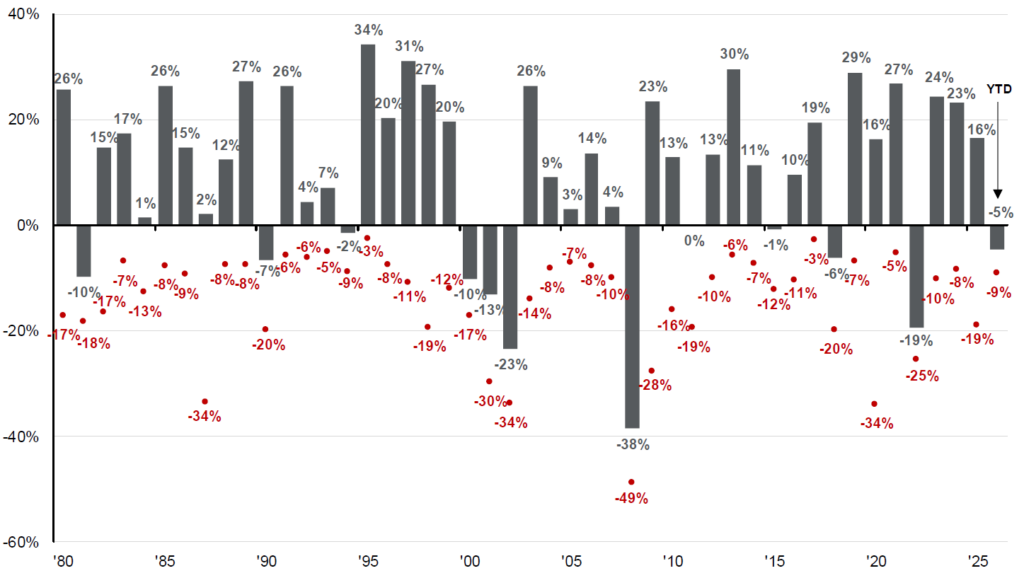

Market Drops are Common

The train that’s generally moving up a mountain needs to let out some steam now and again to prevent more serious problems. Going into 2026, the market may have been overheating from strong performance over the past few years. The recent pullback may not be a bad thing as we release some of that pressure.

It serves as a good reminder that market pullbacks are a normal part of investing in the stock market, and the market often ends up on top in the end. Let’s look at the data:

- Market drops are normal: The S&P 500 was up18% in 2025, 25% in 2024 and 26% in 2023. Historically, a market drop of 10% happens just about every year and a drop of 20% happens about every six years. Investors sometimes get comfortable in the good times and forget to expect market turbulence now and then on their way up the mountain.

- Markets are cyclical: Market performance is often overexaggerated on the upside due to excessive expectations and is then overly disappointed as it reverses course. This is why the market is volatile and doesn’t simply move in a straight line. The AI boom exuberance may have been overexaggerated over the past few years, but recent negative geopolitical concerns may have been overstated as well.

- Market drops don’t translate to calendar year losses: Looking at the chart below, in any given year there is often a meaningful market. These losses can be significant — note the 34% drop in 1987, 28% drop in 2009 and 34% drop in 2020 (remember COVID?). What do they have in common? The calendar year return for all those years was positive! Moving out of the market in any one of those years could have led investors to miss out on significant returns. Staying invested through the ups and the downs is the key to long-term investment success.

Annual Returns and Intra-Year Declines

S&P 500 Intra-Year Declines vs. Calendar Year Returns 1980 to Q1 2026

Source: J.P. Morgan Asset Management Guide to the Markets 1Q 2026 as of March 31, 2026. Source: FactSet, Standard & Poor’s, J.P. Morgan Asset Management. Returns are based on price index only and do not include dividends. Intra-year drops refers to the largest peak-to-trough decline during the year. Returns shown are calendar year returns from 1980 to 2025, over which the average annual return was 10.7%. Past performance is no guarantee of future results. Guide to the Markets – U.S. Data are as of March 31, 2026.

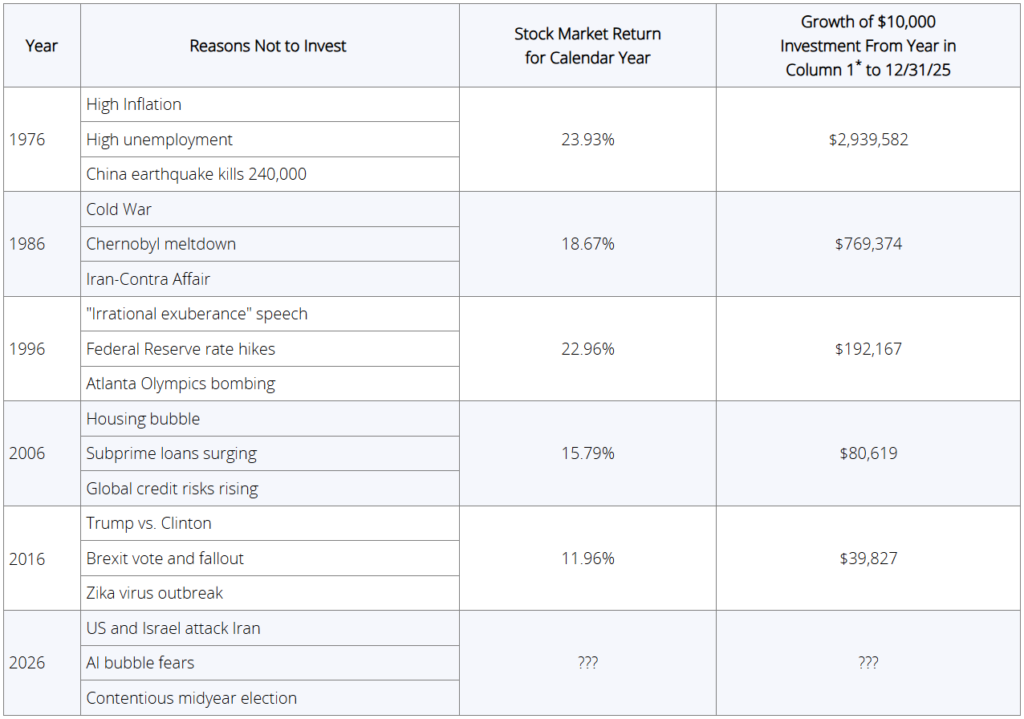

Always Reasons Not to Invest

Regardless of whether the market is going up or down, there are always reasons not to invest. It’s as easy as opening your favorite news site and reading the first few headlines. Remember, bad news sells a lot better than good news. But the main question is, how much impact do geopolitical events really have on long-term market returns?

The chart below looks at each decade over the past 50 year and highlights some of the key events that could have been reasons not to invest in those years. It also shows the market return that year, as well as an illustration of how an investment would grow if held through today. Let’s review the results:

- Always a Reason. There’s a wide range of economic, environmental and geopolitical events on the list, including high inflation, Cold War and the housing bubble. While each year lists three significant events, there could be many more missing. Looking at the list, any one of these events could derail the market, and yet annual returns tell a different story.

- Market is Resilient. In all the years evaluated, the stock market ended the year in positive territory. In fact, all the years posted double-digit returns. While this is a small sample size, the point of the story is that these major events did not derail markets. If investors got out of the market because of one of these events, or due to a short-term market drop caused by the event, they may have missed significant upside on the rebound.

- It’s a Long-Term Game. Looking at the column on the right (Growth of $10,000), the number gets exponentially larger further in history. The power of compounding cannot be overlooked, but it only works if you stay invested. Shifting in and out of the market based on headlines can have a detrimental effect on long-term returns. Staying diversified and invested for the long-term is the best way to increase the chances of reaching investment goals.

Staying Invested Despite Negative News

Source: Hartford Funds, “There Are Always Reasons Not to Invest,” January 2026. Past performance does not guarantee future results. *Assumes an initial investment of $10,000 in stocks beginning on January 1 of the year in column 1 through Dec. 31, 2025, reinvestment of dividends and capital gains, and no taxes or transaction costs. Stocks are represented by the S&P 500 Index, which is a market capitalization-weighted price index composed of 500 widely held common stocks. Indices are unmanaged and not available for direct investment. For illustrative purposes only. Data Sources: Morningstar and Hartford Funds, January 2026.

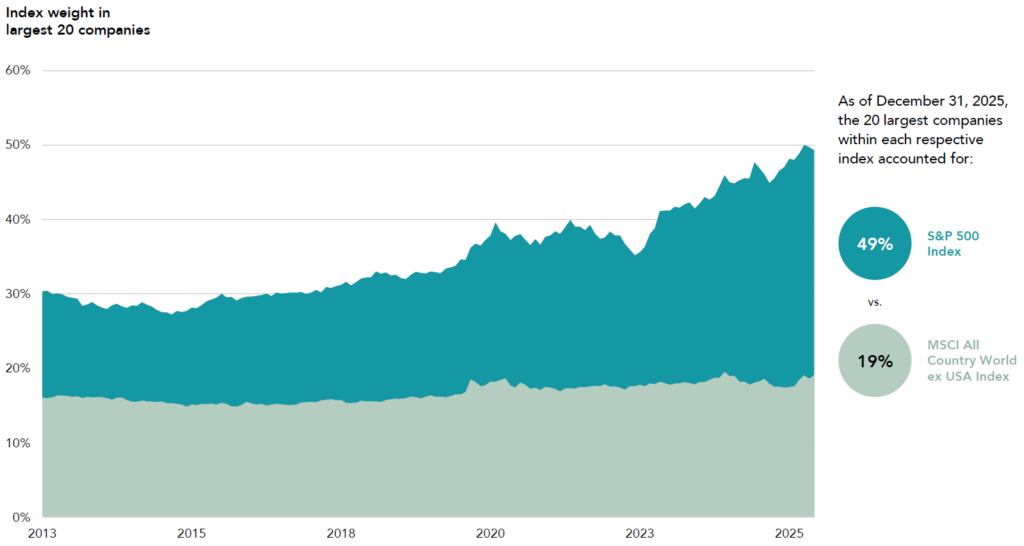

Diversification is Your Seatbelt

If the stock market is like a roller-coaster with constant ups and downs, then diversification is like a seatbelt, keeping you secured to make sure you finish the ride. In this analogy, getting spooked and out of the market would be the equivalent of falling off the ride, a worst-case scenario.

But even when you are investing in a broad market exposure, represented by hundreds of stocks, you may unknowingly become less diversified through certain market concentrations. How can diversification protect you in these scenarios? Let’s explore by looking at concentrations over time for the U.S. versus international markets:

- High Concentration in U.S. The largest 20 companies in the S&P 500 (which is a market-capitalization weighted index of the 500 largest U.S. companies) currently represent almost 50% of the entire index. This is meaningfully higher than sub-30% levels a decade ago and doesn’t leave much room for the other 480 companies. And it means if you only invested in the S&P 500, your portfolio returns were heavily dependent on just those 20 companies. Think about a situation where a disruptive new technology is introduced and one of those companies’ primary products is made obsolete; that stock could plummet, and your portfolio would be subject to significant concentration risk.

- Markets Balanced Abroad. International markets, on the other hand, have less than 20% in their top 20 companies, relatively consistent with where they have been over the past 10 years. This can be attributable to not only a larger investable universe of companies (a lot more than 500), but also a wider range of countries with unique economies and growth potential. There is a much lower risk of any one company derailing your portfolio.

- Diversification is Important. So, which is better to invest in, the U.S. market or international? The beauty of diversification is you don’t have to choose. It’s always best to be diversified across the globe, in a variety of regions and asset classes. Diversification offers a smoother ride for the investor, regardless of market conditions in a specific country or what may be happening with a specific company. A smoother ride offers the comfort needed to stay seated and invested for the long run, ensuring that investors reach the end of their ride.

Stay diversified, my friends.

Global Market Concentration Comparison

Weight in Largest 20 Companies in U.S. vs. International Markets

Jan. 1, 2013–Dec. 31, 2025

Source: Dimensional. Weight determined by constituent percentage of each respective index at the issuer level. Diversification neither assures a profit nor guarantees against loss in a declining market. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. S&P data © 2026 S&P Dow Jones Indices LLC, a division of S&P Global. MSCI data © MSCI 2026, all rights reserved.

As always, Dynamic recommends staying balanced, diversified and invested. Despite short-term market pullbacks, it’s more important than ever to focus on the long-term, improving the chances for investors to reach their goals.

Should you need help navigating client concerns, don’t hesitate to reach out to Dynamic’s Asset Management team at (877) 257-3840, ext. 4 or investmentmanagement@dynamicadvisorsolutions.com.

Disclosures

This commentary is provided for informational and educational purposes only. The information, analysis and opinions expressed herein reflect our judgment and opinions as of the date of writing and are subject to change at any time without notice. This is not intended to be used as a general guide to investing, or as a source of any specific recommendation, and it makes no implied or expressed recommendations concerning the manner in which clients’ accounts should or would be handled, as appropriate strategies depend on the client’s specific objectives.

This commentary is not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. Investors should not assume that investments in any security, asset class, sector, market, or strategy discussed herein will be profitable and no representations are made that clients will be able to achieve a certain level of performance, or avoid loss.

All investments carry a certain risk and there is no assurance that an investment will provide positive performance over any period of time. Information obtained from third party resources are believed to be reliable but not guaranteed as to its accuracy or reliability. These materials do not purport to contain all the relevant information that investors may wish to consider in making investment decisions and is not intended to be a substitute for exercising independent judgment. Any statements regarding future events constitute only subjective views or beliefs, are not guarantees or projections of performance, should not be relied on, are subject to change due to a variety of factors, including fluctuating market conditions, and involve inherent risks and uncertainties, both general and specific, many of which cannot be predicted or quantified and are beyond our control. Future results could differ materially and no assurance is given that these statements or assumptions are now or will prove to be accurate or complete in any way.

Past performance is not a guarantee or a reliable indicator of future results. Investing in the markets is subject to certain risks including market, interest rate, issuer, credit and inflation risk; investments may be worth more or less than the original cost when redeemed.

Investment advisory services are offered through Dynamic Advisor Solutions, LLC, dba Dynamic Wealth Advisors, an SEC registered investment advisor.