Download the 12.6.24 Bond Market Update for advisors’ use with clients

By Bill Smith, Fixed Income Trader and Portfolio Manager

The Federal Reserve (Fed) has lowered interest rates by 75 basis points since initiating its easing campaign, reducing the federal funds rate to 4.50 – 4.75% from a multi-decade high of 5.25 – 5.50% in September. During this period, inflation has ticked up slightly, and the labor market has remained resilient. Against this backdrop, debates regarding the need for further cuts have ensued. However, numerous comments from Fed officials this week seem to reinforce a general bias towards lower rates moving forward, albeit with plenty of hedging:

“Over the next year, it feels to me like rates come down a fair amount from where they are now, but we meet every six weeks because the conditions change.”

- Austan Goolsbee, Chicago Fed President, Dec. 3, 2024

“At present, I lean toward supporting a cut to the policy rate at our December meeting. But that decision will depend on whether data that we will receive before then surprises to the upside and alters my forecast for the path of inflation.”

- Christopher Waller, Federal Reserve Governor, Dec. 2, 2024

“In order to keep the economy in a good place, we have to continue to recalibrate policy. Now, whether it will be in December or sometime later, that’s a question we’ll have a chance to debate and discuss at our next meeting.”

- Mary Daly, San Francisco Fed President, Dec. 2, 2024

At present, the futures market is telegraphing a similar outlook, with the odds of another cut at the Fed’s next meeting on December 18 sitting around 77% with a full 75 basis points of easing expected by the end of next year, as estimated by Bloomberg’s interest rate probability model. While the future path of monetary policy is always uncertain, further easing remains our base case as we move into 2025.

Yields Remain Elevated

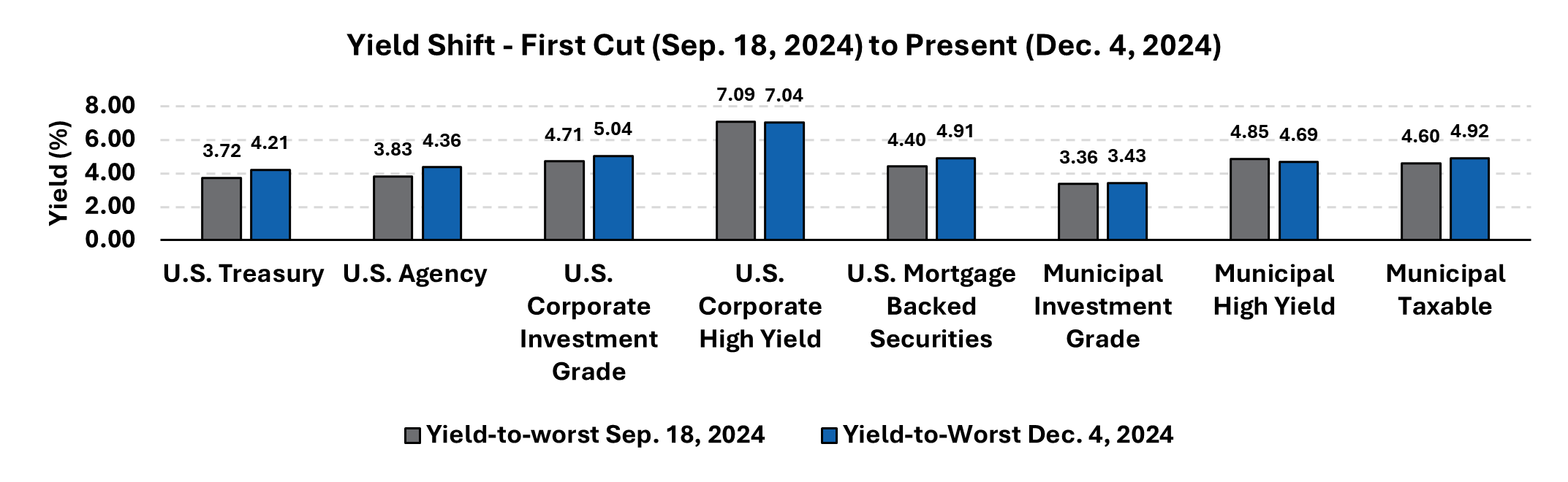

Despite rate cuts, yields have chopped higher across most investment-grade fixed income sectors as shown in the “Yield Shift” chart below. For example, the Bloomberg U.S. Aggregate Index has seen its yield-to-worst rise nearly 50 basis points from 4.17% to 4.66% in the 53 trading days since the Fed started cutting. A large driver of this move continues to be the market’s recalibration of easing expectations. While cuts are still expected, they may come at a slower pace than initially anticipated.

Source: ICE DATA INDICES, LLC (“ICE DATA”), 4 December 2024. Past performance is no guarantee of future results. U.S. Treasury = ICE BofA US Treasury Index, U.S. Agency = ICE BofA US Agency Index, U.S. Corporate Investment Grade = ICE BofA US Corporate Index, U.S. Corporate High Yield = ICE BofA US High Yield Index, U.S. Mortgage Backed Securities = ICE BofA US Mortgage Backed Securities Index, Municipal Investment Grade = ICE BofA US Municipal Securities Index, Municipal High Yield = ICE US High Yield & Non-Rated Municipal Securities Index, Municipal Taxable = ICE BofA Broad US Taxable Municipal Securities Index.

Source: ICE DATA INDICES, LLC (“ICE DATA”), 4 December 2024. Past performance is no guarantee of future results. U.S. Treasury = ICE BofA US Treasury Index, U.S. Agency = ICE BofA US Agency Index, U.S. Corporate Investment Grade = ICE BofA US Corporate Index, U.S. Corporate High Yield = ICE BofA US High Yield Index, U.S. Mortgage Backed Securities = ICE BofA US Mortgage Backed Securities Index, Municipal Investment Grade = ICE BofA US Municipal Securities Index, Municipal High Yield = ICE US High Yield & Non-Rated Municipal Securities Index, Municipal Taxable = ICE BofA Broad US Taxable Municipal Securities Index.

Protect the Income

This shift presents a compelling opportunity to pick up additional yield at attractive levels across fixed income sectors and maturities. It may be tempting to focus exclusively on short-term bonds until there is more clarity regarding monetary policy, yet these instruments carry higher reinvestment risk. If interest rates trend lower, short investors may be forced to reinvest at lower rates when bonds mature.

As such, an allocation to bonds farther out on the curve might be appropriate. Longer maturities are more sensitive to interest rates, but two features of individual bonds should help investors weather future price volatility:

- Bonds Mature at Par: One of the most important aspects of fixed income investing is also the simplest. Bonds mature at par (face value). For buy-and-hold investors, unrealized gains and losses due to shifting interest rates can largely be ignored. Barring a default or bond call, no matter the price volatility experienced over the life of a bond, investors principal is returned at maturity.

- Income Returns are Always Positive: While prices fluctuate over the life of a bond, one aspect of fixed income investing is constant. Income returns are always positive. Barring a default or bond call, you know how much you are going to make, and you know when you are going to get paid.

A prudent approach to fixed income investing calls for diversification across both credit and duration exposure. As always, Dynamic recommends staying balanced, diversified and invested. Despite short-term market pullbacks, it’s more important than ever to focus on the long-term, improving the chances for investors to reach their goals.

Should you need help navigating fixed income for your clients, please contact Dynamic’s Investment Management team at (877) 257-3840, ext. 4 or investmentmanagement@dynamicadvisorsolutions.com.

Bill Smith serves as president, Portfolio Management & Trading, of Harmont Fixed Income in Phoenix.

Disclosures

This commentary is provided for informational and educational purposes only. The information, analysis and opinions expressed herein reflect our judgment and opinions as of the date of writing and are subject to change at any time without notice. This is not intended to be used as a general guide to investing, or as a source of any specific recommendation, and it makes no implied or expressed recommendations concerning the manner in which clients’ accounts should or would be handled, as appropriate strategies depend on the client’s specific objectives.

This commentary is not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. Investors should not assume that investments in any security, asset class, sector, market, or strategy discussed herein will be profitable and no representations are made that clients will be able to achieve a certain level of performance, or avoid loss.

All investments carry a certain risk and there is no assurance that an investment will provide positive performance over any period of time. Information obtained from third party resources are believed to be reliable but not guaranteed as to its accuracy or reliability. These materials do not purport to contain all the relevant information that investors may wish to consider in making investment decisions and is not intended to be a substitute for exercising independent judgment. Any statements regarding future events constitute only subjective views or beliefs, are not guarantees or projections of performance, should not be relied on, are subject to change due to a variety of factors, including fluctuating market conditions, and involve inherent risks and uncertainties, both general and specific, many of which cannot be predicted or quantified and are beyond our control. Future results could differ materially and no assurance is given that these statements or assumptions are now or will prove to be accurate or complete in any way.

Past performance is not a guarantee or a reliable indicator of future results. Investing in the markets is subject to certain risks including market, interest rate, issuer, credit and inflation risk; investments may be worth more or less than the original cost when redeemed.

Investment advisory services are offered through Dynamic Advisor Solutions, LLC, dba Dynamic Wealth Advisors, an SEC registered investment advisor.

Photo: Adobe StockPHN0eWxlPgouZnVzaW9uLWJ1aWxkZXItcm93LTIgIHsKICBiYWNrZ3JvdW5kLXBvc2l0aW9uOiAyNSUgMjUlICFpbXBvcnRhbnQ7Cn0gIAo8L3N0eWxlPg==