Download the 2.21.25 Dynamic Market Update for advisors’ use with clients

By Kostya Etus, CFA®, Chief Investment Officer, Dynamic Asset Management

Broken record here… The stock market (as measured by the S&P 500) hit another all-time-high last week, despite getting an inflation reading above expectations as well as more tariff noise. Market resilience continues as investors turn their heads from the headlines and focus on fundamentals. Companies are making money and reporting strong earnings, and this is happening all over the globe. In fact, the often-overlooked international markets are gaining strength and are the surprise winners so far this year as they regain their footing after a poor performance last quarter.

Perhaps the biggest surprise is that the bond market was up for the fifth straight week, highlighting the run-up in rates late last year may have been overblown. Three things to keep in mind as we look ahead:

- Inflation Above Expectations. The January report for the consumer price index (CPI) came in higher than expected at 3% year-over-year. This was primarily driven by the more volatile food and energy prices. Particularly food prices which increased the most in two years. For example, eggs jumped 15% due to avian influenza or bird flu. Core inflation (which excludes food and energy) ticked up only slightly to 3.3% and remains rangebound.

- Fed is Comfortable. Federal Reserve (Fed) Chair Jerome Powell stated they view the current policy as restrictive, meaning more rate cuts are likely in the future. But given there is more work to be done on lowering inflation, the Fed is comfortable taking its time to achieve their target interest rate levels. Latest expectations suggest cuts may not occur until October.

- Rotation of Fortunes. While high flying tech stocks have dominated the markets over the past couple of years, often referred to as the “Magnificent 7,” they may be starting to come back down to Earth. Earnings and sales growth have slowed and lofty valuations are making investors cautions. On the other hand, growth for the other 493 companies is accelerating. Similarly, beaten up international markets may be making a resurgence as economic conditions may rebound as geopolitical risks subside.

Despite having slightly higher inflation, the Fed maintains their dovish stance and does plan for more rate cuts in the future, albeit more patiently. More importantly, strong earnings continue to drive markets and may also turn the tables on past winners as beaten-up companies re-emerge from their undervalued levels. As always, diversification will be key in this environment.

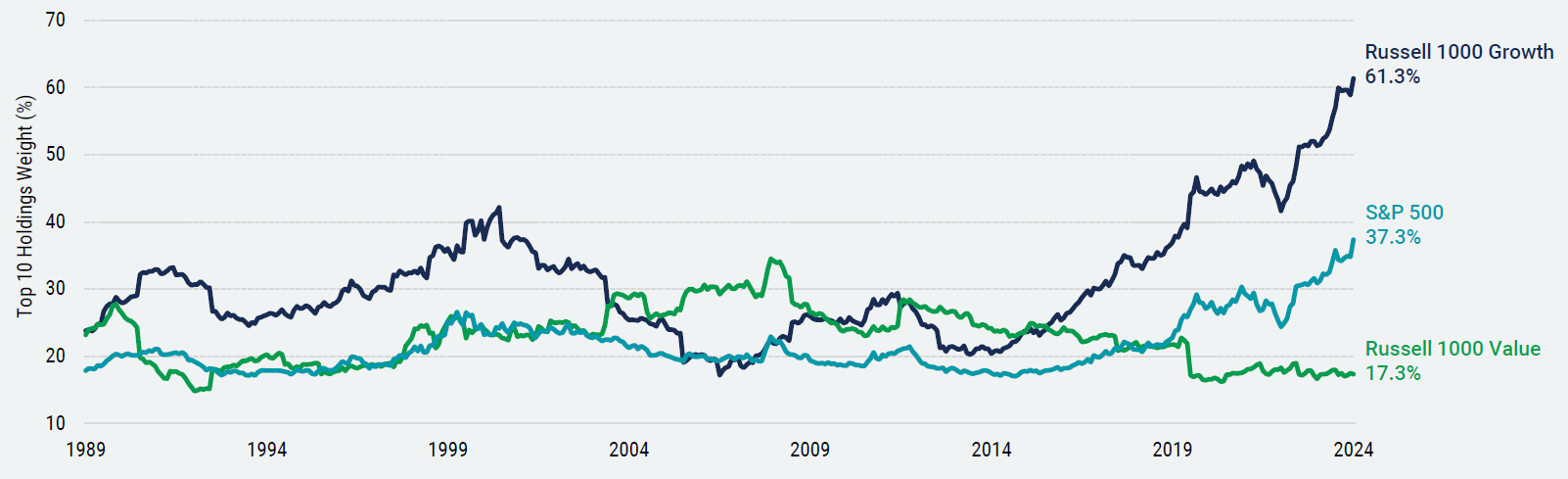

Concentration Risk at Record Highs, but Not Everywhere…

As we all know, the artificial intelligence (AI) boom has led to very concentrated market leadership. Meaning that only a handful of companies are driving market returns, which has led to their weights being excessive within broad-based indexes. The risk is that as these companies increase in weight, a drop in any one company has a bigger impact on the overall portfolio. And given these companies are overvalued, a market correction may have a more significant impact on them on the way down.

Is this concentration exhibited everywhere? The chart below shows the concentration levels of three key indexes:

- S&P 500 Concentration. The weight of the top ten holdings in the S&P 500 index is at an all-time high, with just over a 37% weight at the end of 2024. This only leaves 63% for the other 490 holdings. This is the highest concentration level over the past 35 years. Investors in the S&P 500 need to be cautious of a market correction as it will be highly dependent on fewer companies, meaning diversification benefits have been eroded.

- Russell 1000 Growth Concentration. Looking at only growth companies, more than 61% are in the top ten. This is almost 20% higher than the concentrations we saw during the tech bubble in 2000. At these extreme levels, investing may seem more like stock-picking because investors are heavily exposed to, and dependent on, the performance of only 10 or so companies. There is very little diversification here, and if any of the top companies waver, it could bring down an entire portfolio.

- Russell 1000 Value Concentration. The concentration levels in the value index, on the other hand, is at about the lowest levels it has ever been. This means there are a lot more companies which can benefit overall returns as they rebound off undervalued levels. Additionally, the risk of portfolio loss from any one company falling has been significantly reduced. Overall, in these types of environments of extreme valuations, it is always recommended to stay globally diversified and balanced among various asset classes to improve your chances of investment success.

Stay diversified, my friends.

Top 10 Weight in U.S. Large Cap Indexes

Over the Last 35 Years

Source: Avantis Investors publication of Monthly ETF Field Guide for January 2025. Data from 12/31/1989 – 12/31/2024 from Morningstar. Past performance is no guaranteed of future results.

As always, Dynamic recommends staying balanced, diversified and invested. Despite short-term market pullbacks, it’s more important than ever to focus on the long-term, improving the chances for investors to reach their goals.

Should you need help navigating client concerns, don’t hesitate to reach out to Dynamic’s Asset Management team at (877) 257-3840, ext. 4 or investmentmanagement@dynamicadvisorsolutions.com.

Disclosures

This commentary is provided for informational and educational purposes only. The information, analysis and opinions expressed herein reflect our judgment and opinions as of the date of writing and are subject to change at any time without notice. This is not intended to be used as a general guide to investing, or as a source of any specific recommendation, and it makes no implied or expressed recommendations concerning the manner in which clients’ accounts should or would be handled, as appropriate strategies depend on the client’s specific objectives.

This commentary is not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. Investors should not assume that investments in any security, asset class, sector, market, or strategy discussed herein will be profitable and no representations are made that clients will be able to achieve a certain level of performance, or avoid loss.

All investments carry a certain risk and there is no assurance that an investment will provide positive performance over any period of time. Information obtained from third party resources are believed to be reliable but not guaranteed as to its accuracy or reliability. These materials do not purport to contain all the relevant information that investors may wish to consider in making investment decisions and is not intended to be a substitute for exercising independent judgment. Any statements regarding future events constitute only subjective views or beliefs, are not guarantees or projections of performance, should not be relied on, are subject to change due to a variety of factors, including fluctuating market conditions, and involve inherent risks and uncertainties, both general and specific, many of which cannot be predicted or quantified and are beyond our control. Future results could differ materially and no assurance is given that these statements or assumptions are now or will prove to be accurate or complete in any way.

Past performance is not a guarantee or a reliable indicator of future results. Investing in the markets is subject to certain risks including market, interest rate, issuer, credit and inflation risk; investments may be worth more or less than the original cost when redeemed.

Investment advisory services are offered through Dynamic Advisor Solutions, LLC, dba Dynamic Wealth Advisors, an SEC registered investment advisor.

Photo: Adobe Stock