Download the 7.28.23 Dynamic Market Update for advisors’ use with clients

By Kostya Etus, CFA®, Chief Investment Officer, Dynamic Investment Management

Market Expectations

We had a big week in terms of announcements with back-to-back key updates:

Wednesday, July 26: The U.S. Federal Reserve (Fed) approved a much-anticipated interest rate hike of 0.25% to an overall target range of 5.25%-5.50%. The midpoint of this range marks the highest level of rates in 22 years (since early 2001).

Thursday, July 27: The U.S. Bureau of Economic Analysis reported second quarter Gross Domestic Product (GDP) growth of 2.4%, beating consensus estimates between 1.8%-2.0%. GDP is a prominent measure of economic growth, and this follows the 2.0% growth from the first quarter, which also beat expectations. While there may still be a recession on the horizon, these GDP figures may be indicating a softer downturn.

Another surprising statistic is the Dow Jones Industrial Average (Dow) has been up for 13 consecutive trading days (as of the end of July 26th). This matches the longest winning streak set in 1987.

Markets are benefiting from three key reasons:

- Decreased expectations of a recession (at least a severe one).

- Strong corporate earnings which are beating expectations.

- Increased expectations of no additional rate hikes.

The last reason is perhaps the most important factor for both stock and bond market outlooks. There are two primary views on future interest rates:

- Federal Open Market Committee (FOMC) Projections: On a quarterly basis, when the Fed meets, each member indicates their view of the midpoint of the range for the federal funds rate at the end of each of the next three years and over the long run. The median of these expectations is viewed as the expected rate. This is commonly referred to as the “Fed Dot Plot”.

- Market Expectations: At any time, a market-implied probability for future fed funds rates can be calculated based on future and forward contracts on overnight financing rates, often referred to as Secured Overnight Financing Rate (SOFR).

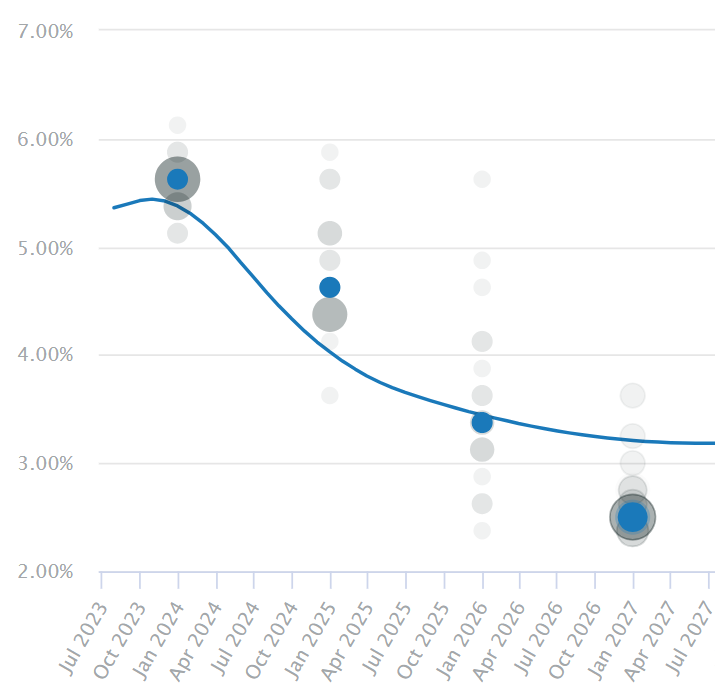

Below is the current comparison between the FOMC projections and market expectations. What you will notice is both measures are indicating holding steady for the remainder of 2023 and expecting rate cuts in 2024. Market expectations are implying that rate cuts can begin as early as February and by the end of the year could be down to a target of about 4%. That would equate to potentially five or six 0.25% rate cuts by the Fed in 2024. This could be supporting for economic growth as well as a tailwind for both stock and bond markets.

Fed Funds Implied Rate: FOMC Projections vs. Market Expectations

Grey Dots: Fed Dot Plot Projections

Blue Dots: Fed Median Projections

Blue Line: Market-Implied 3-Month Term SOFR

Source: Obtained from Chatham Financial as of July, 26, 2023. Past Results are not predictive of results in future periods.

Market Concentrations

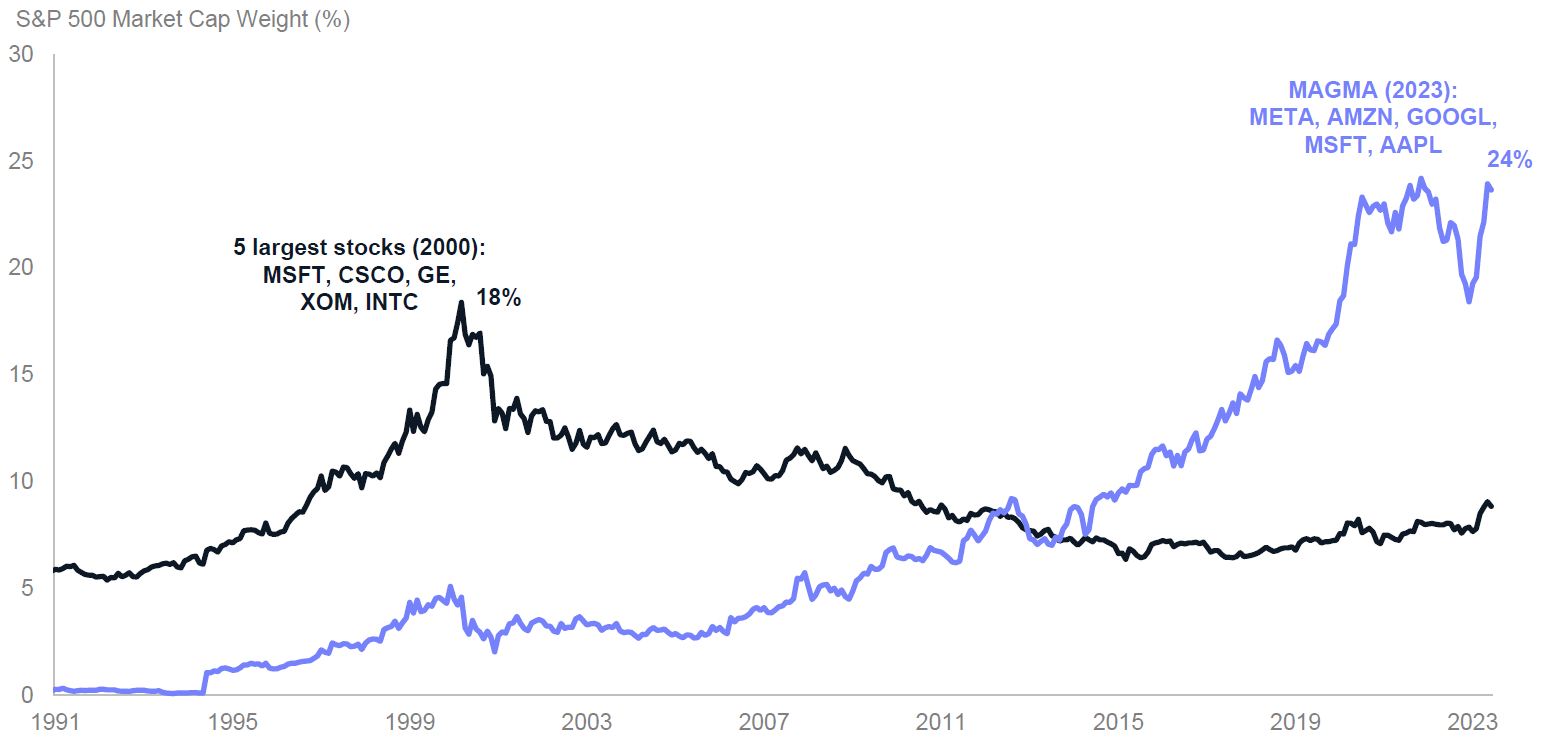

Yet another surprising statistic this week: The five largest companies in the S&P 500 Index make up about 24% of the index’s market value (as of June 30, 2023), nearing a historical high. This may present material risk for investors.

We have witnessed high levels of S&P 500 Index concentration before, around the Dot-Com Bubble (see graph below), and it did not bode well for most of those concentrated positions as time went on.

The graph below indicates how the current concentrations compare to those in 2000, and how those holdings have changed over time. Here are the key observations:

- Concentration Risk: From a risk standpoint, having too much allocated to a single asset class is bad, a single sector is worse, and a single stock is perhaps the worst. The more granular an exposure, the more risk there is. For example, a single company might go bankrupt due to a change in consumer preferences or technological innovation, cause an environmental disaster, get involved in a scandal, or simply fall out of favor with investors. If your concentrated position tanks, it can bring down your portfolio with it.

- Market-Cap Weighting Risk: Investing in a fund holding many companies helps to protect from concentration risk, but you have to be mindful of the fund you select. The S&P 500 Index holds the 500 largest companies in the U.S., that sounds diversified, right? But the holdings in the index are market-cap weighted, meaning the stocks it holds are weighted based on total market value of each firm. Thus, if any company stock price grows faster than others, its weight grows also. Now what if only a few companies grow? Then you get a quarter of the index invested in five stocks! That doesn’t leave much room for the other 495 and you are subject to concentration risk once again.

- Diversification of Risk: Selecting funds that do not use market-cap weighting helps to diversify concentration risk. One of the more common approaches is to equal-weight, meaning each holding in the S&P 500 would have the same weight. Alternatively, a better approach could be to employ factor investing. Instead of weighting stocks based on price, weight them based on factors which have proven to help companies grow: attractive valuations, higher quality, stronger momentum, and lower volatility to name a few. Avoiding concentration risk and maximizing diversification benefits can help support more stable returns and ultimately boost risk-adjusted returns over the long-term.

Stay diversified, my friends.

Market Concentration

(Top 5 Stocks in the S&P 500: 2000 vs. 2023)

Sources: Bloomberg, Goldman Sachs Global Investment Research, and Goldman Sachs Asset Management as of June 30, 2023. Chart shows the market capitalization of 5 mega cap companies in the S&P 500 Index as a percent of the total market capitalization of the Index. “MAGMA” is an acronym that refers to those five mega cap companies (META, AMZN, GOOGL, MSFT, and AAPL). Any reference to a specific company or security does not constitute a recommendation to buy, sell, hold or directly invest in the company or its securities. It should not be assumed that investment decisions made in the future will be profitable or will equal the performance of the securities discussed in this document. Past performance does not guarantee future results, which may vary.

As always, Dynamic recommends staying balanced, diversified and invested. Despite short-term market pullbacks, it’s more important than ever to focus on the long-term, improving the chances for investors to reach their goals.

Should you need help navigating client concerns, don’t hesitate to reach out to Dynamic’s Investment Management team at (877) 257-3840, ext. 4 or investmentmanagement@dynamicadvisorsolutions.com.

Disclosures

This commentary is provided for informational and educational purposes only. The information, analysis and opinions expressed herein reflect our judgment and opinions as of the date of writing and are subject to change at any time without notice. This is not intended to be used as a general guide to investing, or as a source of any specific recommendation, and it makes no implied or expressed recommendations concerning the manner in which clients’ accounts should or would be handled, as appropriate strategies depend on the client’s specific objectives.

This commentary is not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. Investors should not assume that investments in any security, asset class, sector, market, or strategy discussed herein will be profitable and no representations are made that clients will be able to achieve a certain level of performance, or avoid loss.

All investments carry a certain risk and there is no assurance that an investment will provide positive performance over any period of time. Information obtained from third party resources are believed to be reliable but not guaranteed as to its accuracy or reliability. These materials do not purport to contain all the relevant information that investors may wish to consider in making investment decisions and is not intended to be a substitute for exercising independent judgment. Any statements regarding future events constitute only subjective views or beliefs, are not guarantees or projections of performance, should not be relied on, are subject to change due to a variety of factors, including fluctuating market conditions, and involve inherent risks and uncertainties, both general and specific, many of which cannot be predicted or quantified and are beyond our control. Future results could differ materially and no assurance is given that these statements or assumptions are now or will prove to be accurate or complete in any way.

Past performance is not a guarantee or a reliable indicator of future results. Investing in the markets is subject to certain risks including market, interest rate, issuer, credit and inflation risk; investments may be worth more or less than the original cost when redeemed.

Investment advisory services are offered through Dynamic Advisor Solutions, LLC, dba Dynamic Wealth Advisors, an SEC registered investment advisor.

Photo: Adobe Stock