Advisors can help create generationally better outcomes through savvy planning

By Lucas Felbel, CIMA®, Director, Portfolio Services

If you’re a young parent, you’ve likely either experienced yourself—or know someone who has—the familial burden that lingering student loan debt can cast over careers, monthly expenses and wealth accumulation. At a time when you may still be grappling with your own student loan debt, you’re likely already thinking about how to finance college for your children at a time when the cost of higher education continues to rise.

In fact, average student loan debt in 2024 for federal student loans was approximately $37,850 in 2024, although individual totals vary considerably.1 If you have small children today, the cost of college is predicted to significantly escalate over the next two decades. For example, if you have a four-year-old who would be likely to start college in 2037, the cost of four years at an in-state college is close to $150,000, according to the Massachusetts Educational Financing Authority.2

In this environment, prudent college planning with a financial advisor may offer opportunities to lessen the burden for the next generation by the time they eventually receive their hard-earned diplomas and pursue career goals. To achieve this outcome, American families are increasingly turning to 529 college savings plans as a strategic financial tool. These plans, named after Section 529 of the Internal Revenue Code, offer a compelling combination of tax advantages, investment growth opportunities, estate planning options, flexibility and control. These benefits make them an attractive component of contemporary college financing strategies.

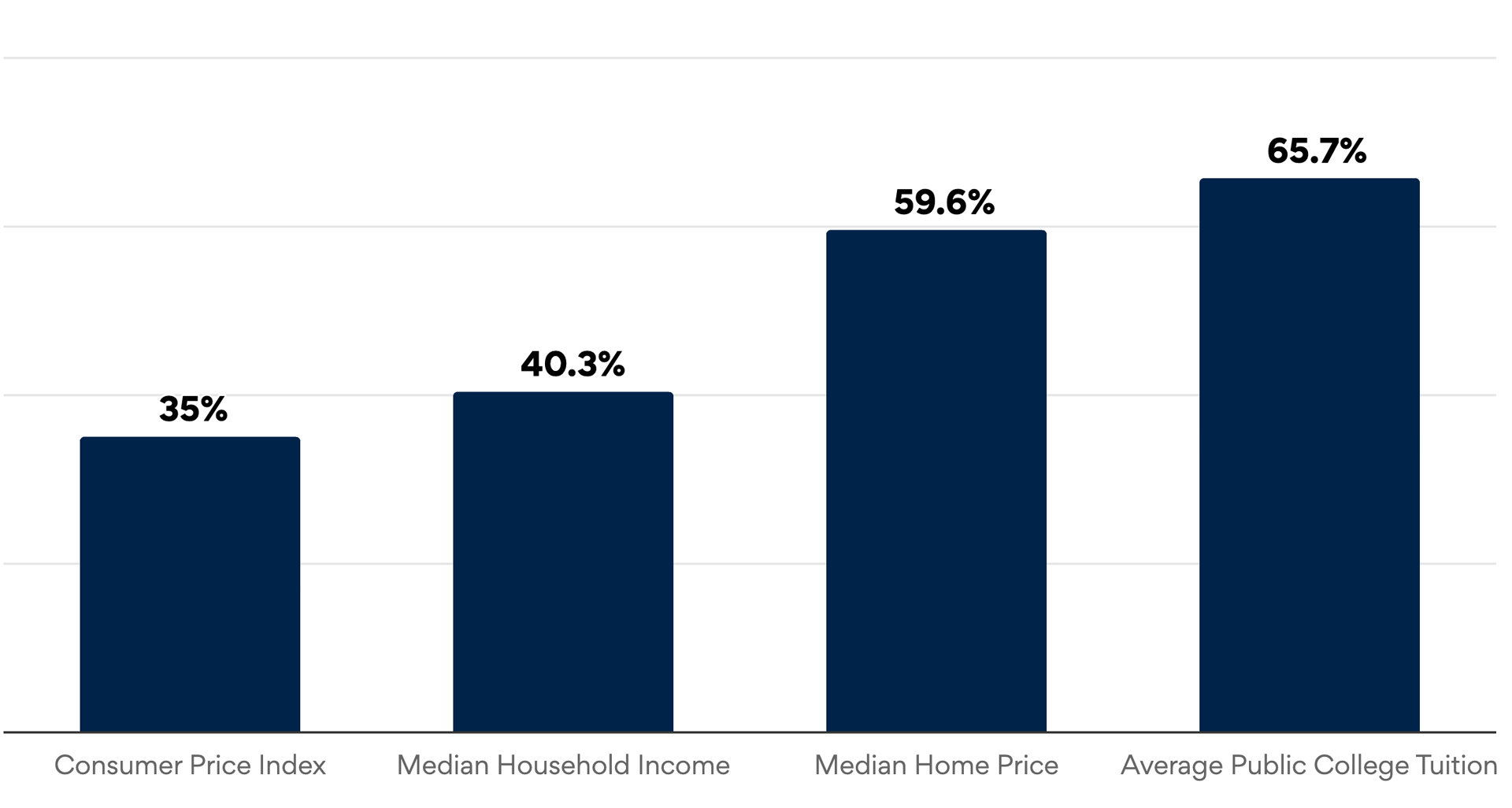

Cost Inflation From 2001-2021

Source: BestColleges.com3

Tax Efficiency: A Core Benefit

One of the foremost benefits of 529 plans is their tax efficiency. Contributions to these plans are made with after-tax dollars, but the investment growth is federally tax-deferred. More significantly, withdrawals used for qualified education expenses—such as tuition, room and board, and required supplies (textbooks, laptops, etc.)—are completely tax-free. Compared to taxable account alternatives, this tax-free growth may enhance the overall return on investment and simplify taxes over decades.

In addition to federal tax advantages, many states offer their own incentives. Over 30 states provide residents with either a tax deduction or credit for contributions made to a 529 plan. While these benefits vary widely in their specifics, they collectively represent a powerful incentive to prioritize 529 contributions.

For example, New York allows a state income tax deduction of up to $10,000 for married couples filing jointly, which can significantly lower the effective cost of contributions in higher state tax states.4 Advisors seeking to add value to their clients’ college planning journey should research the best 529 account for clients given their state of residence and tax situation.

Investment Growth Potential

Another compelling feature is the potential for investment growth. Unlike some other education savings vehicles, 529 plans typically offer a range of investment options, including age-based portfolios that automatically adjust the asset mix as the beneficiary approaches college age. This can provide a balance of growth and risk management, tailored to the time horizon of the student’s educational needs.

Estate Planning Advantages

From an estate planning perspective, 529 plans offer unique benefits. Contributions are considered completed gifts for tax purposes, meaning they can reduce the taxable estate of the contributor while allowing them to retain control of the funds. Contributors can also leverage the “five-year election” to front-load up to five years’ worth of gifts. For example, a married couple can use the $18,000 per year annual gift limit to contribute $180,000 total to one 529 account. Because gift taxes are not triggered under this scenario, grandparents, for example, can make use of this option to manage potential future estate taxes.

Flexibility and Control

529 plans are also deployed for their flexibility. Account holders retain control over the funds, allowing them to change beneficiaries if the original beneficiary opts not to pursue higher education. This feature makes 529 plans not only an effective tool for parents but also for grandparents looking to support their grandchildren’s educational goals. Furthermore, the funds can be used at accredited institutions nationwide, in a limited capacity for private pre-college education, and even at many international universities—expanding the scope and utility of these plans.

Additionally, with the onset of SECURE Act 2.0, unused 529 funds held for 15 years have the added ability to transition up to $35,000 per lifetime per beneficiary to a Roth IRA account which can jumpstart retirement savings and may alleviate potential tax burdens of non-qualified distributions if unused 529 funds cannot be repurposed for another family member.5

529 Plans: A Beacon of Hope

In an era where the burden of student loans looms large, 529 college savings plans emerge as a beacon of hope. Their tax advantages, investment flexibility and estate planning benefits make them an attractive tool for families planning for future educational expenses.

As tuition rates continue to climb, the prudent utilization of 529 plans can make the dream of higher education more attainable for the next generation. Families exercising this strategic foresight provide increased opportunities for young family members to forego the stresses and restrictiveness of pursuing their dreams with cumbersome student debt. Young parents should strongly consider partnering with a trusted financial advisor to discuss how a personalized education savings plan can potentially create generationally better outcomes in their financial plan.

Sources:

- “Average Student Loan Debt: 2024 Statistics,” BestColleges.com, May 30, 2024

- “Estimate Future College Costs with the College Cost Projector,” Massachusetts Educational Financing Authority, 2024

- “College Tuition Inflation Statistics,” BestColleges.com, Oct. 2, 2023

- “Direct Plan Tax Benefits,” NY’s 529 College Savings Program

- “How Unused 529 Assets Can Help with Retirement Planning,” Fidelity.com, May 22, 2024

Invest with Intention.

This article is not exhaustive, and specific advice should be sought from qualified tax professionals before implementation.

Disclosures

This commentary is provided for informational and educational purposes only. The information, analysis and opinions expressed herein reflect our judgment and opinions as of the date of writing and are subject to change at any time without notice. This is not intended to be used as a general guide to investing, or as a source of any specific recommendation, and it makes no implied or expressed recommendations concerning the manner in which clients’ accounts should or would be handled, as appropriate strategies depend on the client’s specific objectives.

This commentary is not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. Investors should not assume that investments in any security, asset class, sector, market, or strategy discussed herein will be profitable and no representations are made that clients will be able to achieve a certain level of performance, or avoid loss.

All investments carry a certain risk and there is no assurance that an investment will provide positive performance over any period of time. Information obtained from third party resources are believed to be reliable but not guaranteed as to its accuracy or reliability. These materials do not purport to contain all the relevant information that investors may wish to consider in making investment decisions and is not intended to be a substitute for exercising independent judgment. Any statements regarding future events constitute only subjective views or beliefs, are not guarantees or projections of performance, should not be relied on, are subject to change due to a variety of factors, including fluctuating market conditions, and involve inherent risks and uncertainties, both general and specific, many of which cannot be predicted or quantified and are beyond our control. Future results could differ materially and no assurance is given that these statements or assumptions are now or will prove to be accurate or complete in any way.

Past performance is not a guarantee or a reliable indicator of future results. Investing in the markets is subject to certain risks including market, interest rate, issuer, credit and inflation risk; investments may be worth more or less than the original cost when redeemed.

Investment advisory services are offered through Dynamic Advisor Solutions, LLC, dba Dynamic Wealth Advisors, an SEC registered investment advisor.

For more information, contact Dynamic’s Investment Management team at (877) 257-3840, ext. 4 or investmentmanagement@dynamicadvisorsolutions.com.

As Director, Portfolio Services, Lucas Felbel, CIMA®, leads the implementation, monitoring and evaluation of trading activities at Dynamic Advisor Solutions.

Photo: Adobe Stock