Download the 9.2.22 Dynamic Market Update for advisors’ use with clients

By Kostya Etus, CFA®, Head of Strategy, Dynamic Investment Management

Recent Market Activity: Volatility Abounds

- Friday, Aug. 26 – Jackson Hole, Wyo.: Federal Reserve (Fed) Chairman Jerome Powell made a clear and direct speech about the Fed’s plans going forward. Fighting inflation is the Fed’s top priority; they’ll continue to raise interest rates and decrease bond purchases “for some time” until they’re confident inflation is under control—even if it’s painful for the economy and markets.

- Stock Market Reaction: The immediate reaction was in fact pain for the market in the form of more than a 3% drop for the S&P 500. And it didn’t stop there, as of this writing (on September 1), the market has fallen for four consecutive days.

- Outlook for Interest Rates: Fed projections suggest that rates would rise to close to 4% through the end of 2023 and they will be mindful to not lower rates too soon. Market priced expectations are now calling for a higher likelihood of another 0.75% hike at the next Fed meeting on September 21 and for rates to finish the year in the 3.75% to 4.00% range (implying more hikes to come).

- Economic Outlook: Rising rates and a more restrictive monetary policy do not bode well for the economy, however, not all is bad news: The labor market is still strong, inflation expectations continue to come down (albeit slowly) and gross domestic product (GDP) growth is expected to be positive in the third quarter.

Additionally, there is another unique market phenomenon, which may be supportive of economic growth, known as the presidential cycle.

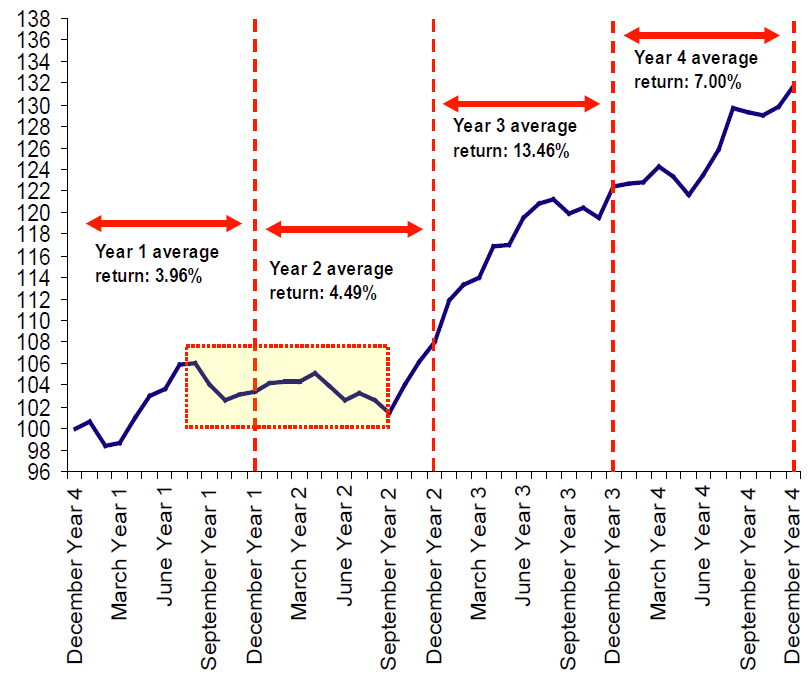

Silver Linings Outlook: How Does the Presidential Cycle Impact the Stock Market?

The chart below shows there’s a unique trend exhibited in the stock market throughout history, depending on which year we’re in based on the four-year presidential cycle, suggesting there may be a link.

- The premise is that the first two years are weaker than the last two. During the first half of a president’s tenure, there is more focus on fulfilling campaign promises, which may not be aimed at strengthening the economy. While in the second half, we re-enter campaign mode with a push to bolster the economy in hopes of seeking a re-election.

- The weakest 12 months… is the last 12 months. Interestingly, we have just experienced the weakest year of the presidential cycle. Notice that after September of the second year, there tends to be a spike as we move into mid-term elections.

- The third year is the strongest. The economy is impacted by many factors, as is the stock market. Monetary policy, dictated by the Fed, has certainly dominated the headlines this year, but it’s important to remember that fiscal policy plays an important role as well. If we see a renewed focus on strengthening the economy from the government, there could be additional support to keep the U.S. out of a recession in 2023.

Historical Presidential Cycle Pattern

Source: Merrill Lynch, Data from 1928 through 2012

Past performance is not indicative of future returns.

As always, Dynamic recommends staying balanced, diversified and invested. Despite short-term market pullbacks, it’s more important than ever to focus on the long-term, improving the chances for investors to reach their goals.

Should you need help navigating client concerns, don’t hesitate to reach out to Dynamic’s Investment Management team at (877) 257-3840, ext. 4 or investmentmanagement@dynamicadvisorsolutions.com.

Disclosures

This commentary is provided for informational and educational purposes only. The information, analysis and opinions expressed herein reflect our judgment and opinions as of the date of writing and are subject to change at any time without notice. This is not intended to be used as a general guide to investing, or as a source of any specific recommendation, and it makes no implied or expressed recommendations concerning the manner in which clients’ accounts should or would be handled, as appropriate strategies depend on the client’s specific objectives.

This commentary is not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. Investors should not assume that investments in any security, asset class, sector, market, or strategy discussed herein will be profitable and no representations are made that clients will be able to achieve a certain level of performance, or avoid loss.

All investments carry a certain risk and there is no assurance that an investment will provide positive performance over any period of time. Information obtained from third party resources are believed to be reliable but not guaranteed as to its accuracy or reliability. These materials do not purport to contain all the relevant information that investors may wish to consider in making investment decisions and is not intended to be a substitute for exercising independent judgment. Any statements regarding future events constitute only subjective views or beliefs, are not guarantees or projections of performance, should not be relied on, are subject to change due to a variety of factors, including fluctuating market conditions, and involve inherent risks and uncertainties, both general and specific, many of which cannot be predicted or quantified and are beyond our control. Future results could differ materially and no assurance is given that these statements or assumptions are now or will prove to be accurate or complete in any way.

Past performance is not a guarantee or a reliable indicator of future results. Investing in the markets is subject to certain risks including market, interest rate, issuer, credit and inflation risk; investments may be worth more or less than the original cost when redeemed.

Investment advisory services are offered through Dynamic Advisor Solutions, LLC, dba Dynamic Wealth Advisors, an SEC registered investment advisor.

Photo: The White House, David Everett Strickler, Unsplash