Lower Inflation, Cooling Labor Market Set the Stage for the Fed

Download the 7.31.24 Dynamic Bond Market Update for advisors’ use with clients

By Bill Smith, Fixed Income Trader and Portfolio Manager

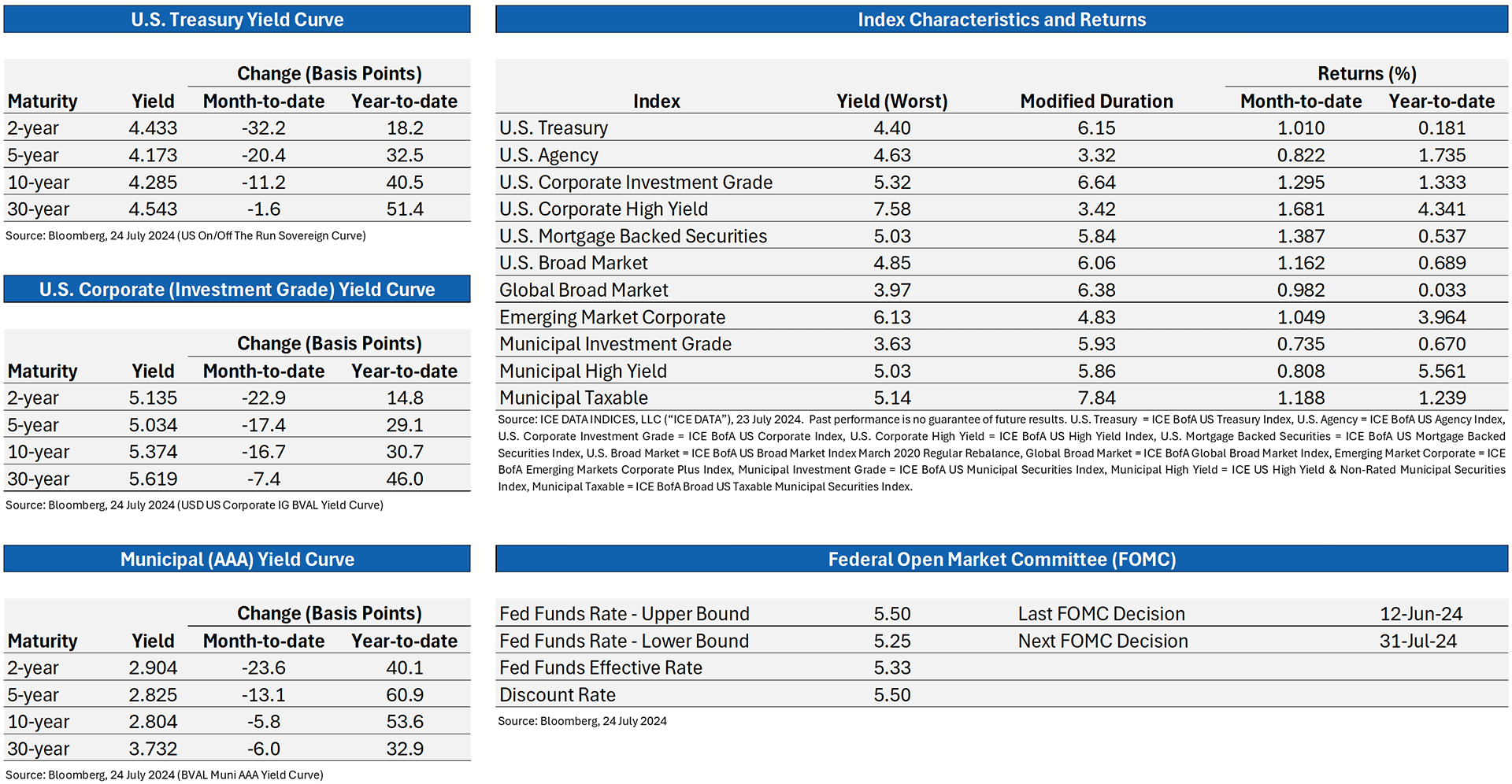

Markets are pricing in significant rate cuts in 2024. Bloomberg’s interest rate probability model estimates two U.S. Federal Reserve (Fed) cuts by November, with a 66% chance of a third by December.* Fixed income markets have responded accordingly, with positive monthly performance seen broadly across most fixed income indices. Long Treasury investors breathed a sigh of relief, at least for now, as the year-to-date performance of the ICE BofA Treasury index turned positive in July. In line with the theme from last month, high-yield municipal, high-yield U.S. corporate and emerging market bonds have continued to outperform this year. The charts, shown below, summarize the yield changes and performance of select fixed income tenors and indices as of July 24.

* “Traders Add to Bets on Three Fed Rate Cuts in 2024,” Bloomberg.com, July 15, 2024

Past performance is no guarantee of future results.

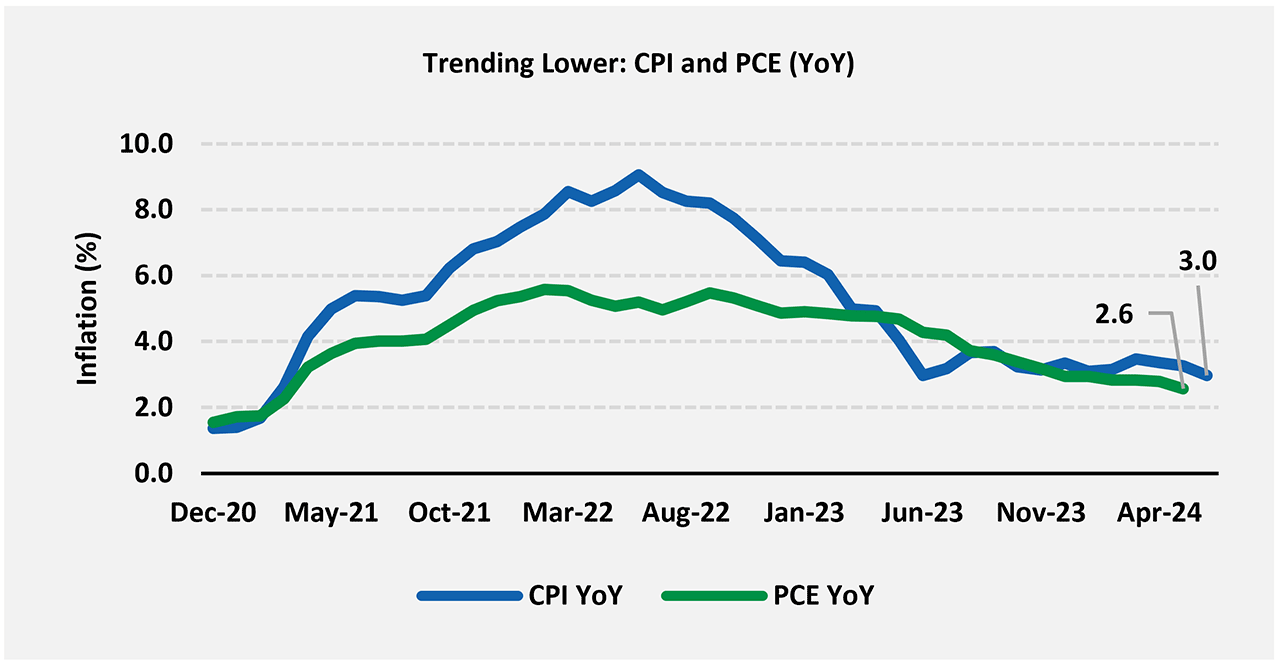

Inflation/Labor Market Snapshot

Inflation is trending lower. On July 15, Jerome Powell reiterated, “If you wait until inflation gets all the way down to 2%, you’ve probably waited too long.” With the consumer price and personal consumption indexes nearing the Fed’s 2% target, the odds of policy easing in the last half of the year are increasing.

Source: Bureau of Labor Statistics, Bureau of Economic Analysis, 25 June 2024. Past performance is no guarantee of future results.

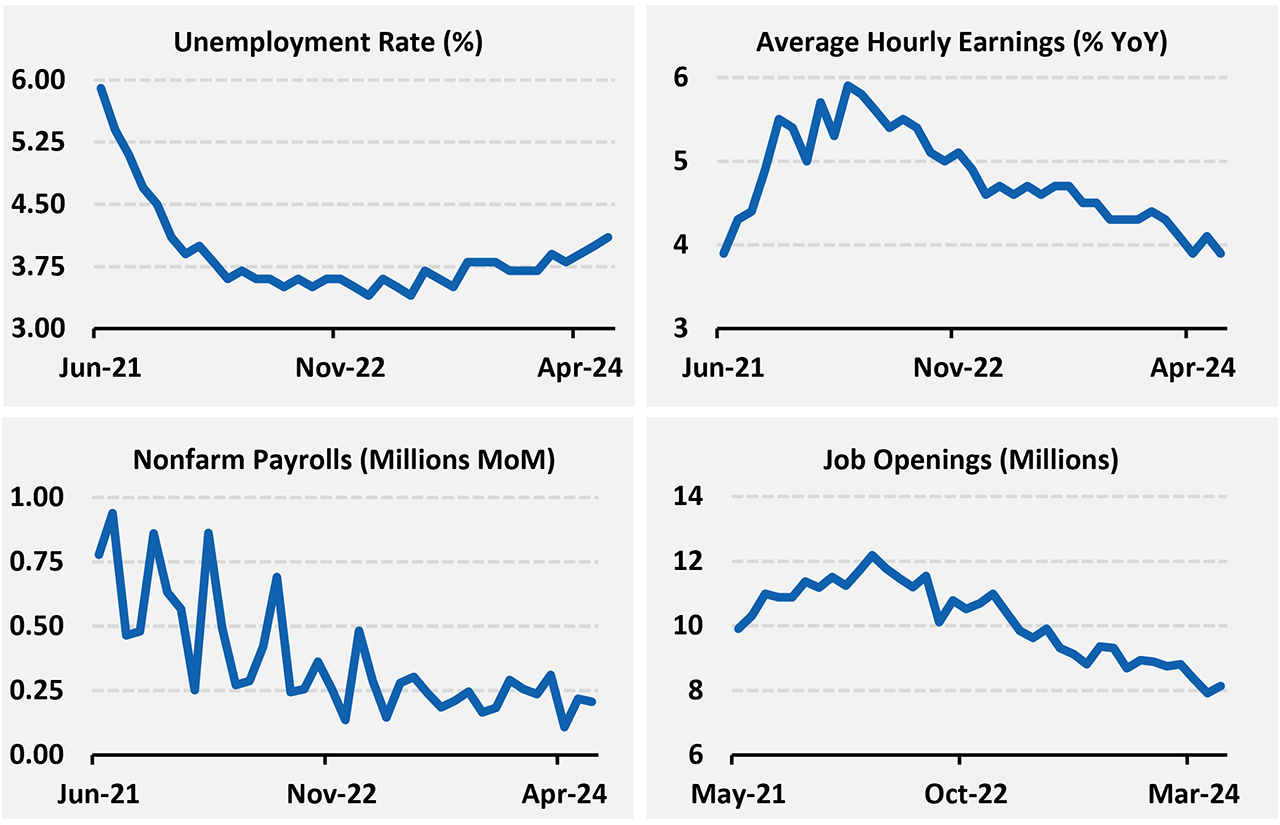

The labor market has softened. Numerous indicators across the job market have weakened in 2024, further bolstering the case for potential rate cuts. Jerome Powell recently noted, “Now that inflation has come down and the labor market has indeed cooled off, we’re going to be looking at both mandates.” Employment data will likely play a larger role in the timing and magnitude of potential rate cuts moving forward.

Source: Bureau of Labor Statistics, 24 July 2024 and Bloomberg News, “Fed Prepares for September Cut as Powell Shifts Focus to Jobs” by Craig Torres and Amara Omeokwe, 17 July 2024.

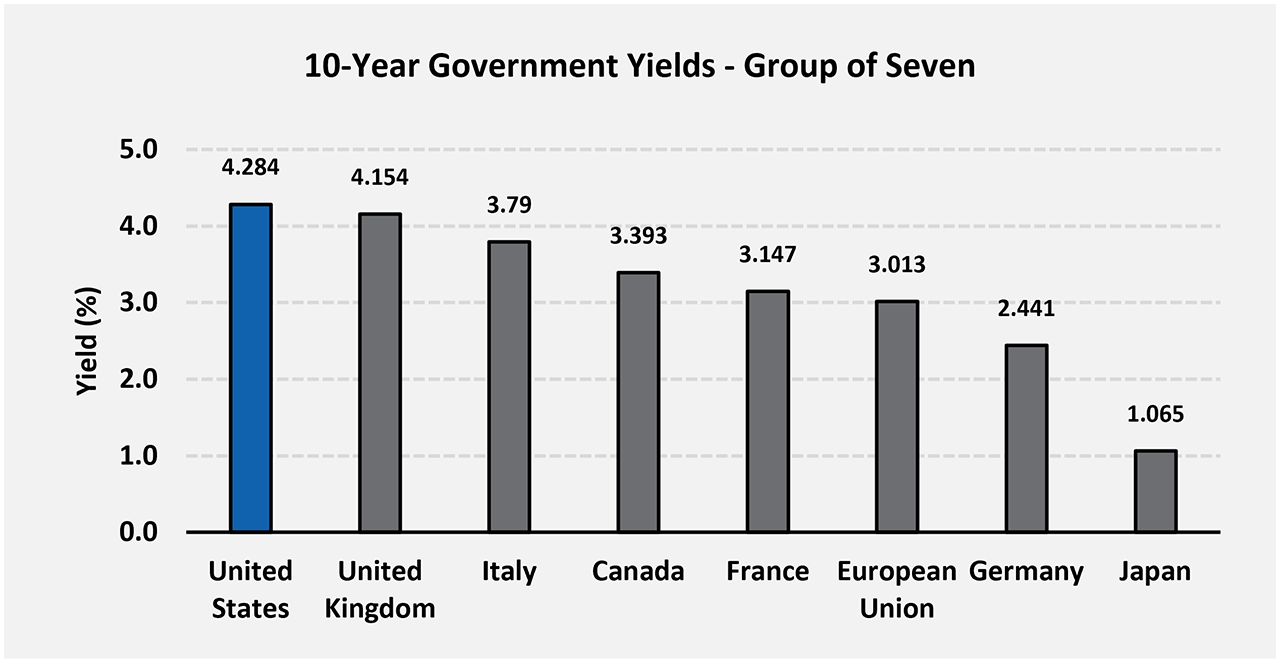

U.S. Yield Snapshot

Yields remain high in the world’s largest government bond market. Even after declining 11 basis points this month, U.S. Treasury yields are still running higher than the debt of every member of the Group of Seven (G-7) across 10-year maturities.

Source: Bloomberg, 24 July 2024. Past performance is no guarantee of future results.

Real yields appear attractive. Yields across major U.S. fixed income indices are now well above the inflation rate. For example, the ICE BofA Treasury Index yields 4.40%, which is 1.40% above last month’s YoY CPI print and 2.00% above the ten-year average of -0.65%.

Source: ICE DATA INDICES, LLC (“ICE DATA”), 24 July 2024. Ten-year average from 06/2014 to 06/2024. Past performance is no guarantee of future results.

A prudent approach to fixed income investing calls for diversification across both credit and duration exposure. As always, Dynamic recommends staying balanced, diversified and invested. Despite short-term market pullbacks, it’s more important than ever to focus on the long-term, improving the chances for investors to reach their goals.

Should you need help navigating fixed income for your clients, please contact Dynamic’s Investment Management team at (877) 257-3840, ext. 4 or investmentmanagement@dynamicadvisorsolutions.com.

Bill Smith serves as president, Portfolio Management & Trading, of Harmont Fixed Income in Phoenix.

Disclosures

This commentary is provided for informational and educational purposes only. The information, analysis and opinions expressed herein reflect our judgment and opinions as of the date of writing and are subject to change at any time without notice. This is not intended to be used as a general guide to investing, or as a source of any specific recommendation, and it makes no implied or expressed recommendations concerning the manner in which clients’ accounts should or would be handled, as appropriate strategies depend on the client’s specific objectives.

This commentary is not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. Investors should not assume that investments in any security, asset class, sector, market, or strategy discussed herein will be profitable and no representations are made that clients will be able to achieve a certain level of performance, or avoid loss.

All investments carry a certain risk and there is no assurance that an investment will provide positive performance over any period of time. Information obtained from third party resources are believed to be reliable but not guaranteed as to its accuracy or reliability. These materials do not purport to contain all the relevant information that investors may wish to consider in making investment decisions and is not intended to be a substitute for exercising independent judgment. Any statements regarding future events constitute only subjective views or beliefs, are not guarantees or projections of performance, should not be relied on, are subject to change due to a variety of factors, including fluctuating market conditions, and involve inherent risks and uncertainties, both general and specific, many of which cannot be predicted or quantified and are beyond our control. Future results could differ materially and no assurance is given that these statements or assumptions are now or will prove to be accurate or complete in any way. Past performance is not a guarantee or a reliable indicator of future results. Investing in the markets is subject to certain risks including market, interest rate, issuer, credit and inflation risk; investments may be worth more or less than the original cost when redeemed.

Investment advisory services are offered through Dynamic Advisor Solutions, LLC, dba Dynamic Wealth Advisors, an SEC registered investment advisor.

Photo: Adobe Stock