Download the 06.26.26 Dynamic Market Update for advisors’ use with clients

By Kostya Etus, CFA®, Chief Investment Officer, Dynamic Asset Management

We have had quite the ride in the markets in June with increased volatility and wild market swings. Volatility has primarily been driven by geopolitics, an artificial intelligence (AI) revaluation and a highly anticipated Federal Reserve (Fed) meeting. But before we dive into the reasons, let’s remember that volatility is a two-way street (markets move up and down) and a natural part of the stock market.

Case in point, cutting through the noise, we find the U.S. market (as measured by the S&P 500) up more than 8% on the year through June 24. Diversified portfolios continue to have a great year with small-caps (+21%), international markets (+13%) and real estate (+12%) continuing to outperform.

Let’s review the three primary drivers of volatility and what they may mean for the markets moving forward:

- The Good: The memorandum of understanding drives potential for lower inflation. On June 14, President

Trump announced the signing of an agreement with Iran, potentially bringing the Iran war to a close. While nobody knows the long-term geopolitical implications of this deal, most relevant for investors is the shorter-term path to reopening the Strait of Hormuz, allowing oil to leave the Persian Gulf. This is important from a macroeconomic standpoint because oil prices have been driving inflation higher over the past several months, creating uncertainly over future interest rate moves from the Fed. The market reaction has been a drop in oil prices with crude oil now trading close to $70 per barrel — the lowest levels since the start of March and well below the $80 to $110 range we’ve had since then.

- The Bad: New Fed chair is more hawkish than expected. “Hawkish” and “dovish” are terms used to describe a stance on monetary policy: Hawks prioritize fighting inflation with higher rates, while a doves focus on lower rates to boost economic growth. The Fed held their first meeting with newly appointed Kevin Warsh at the helm, replacing Jerome Powell. Leading up to the meeting, the expectation was for Warsh to take a more dovish stance in support of the economy. This was not the case. Rates were held unchanged at the meeting, as expected, but future expectations of a rate cut in 2026 were removed and instead replaced with a potential rate hike before year end based on higher inflation expectations. This sent longer-dated interest rates higher, adding a headwind for financial markets.

- The Ugly. The great revaluation of tech stocks. Mega-cap growth companies have been the market leaders over the past couple years, driven by the AI boom. But with valuations getting stretched for these high-flying technology companies, investors are starting to question the mounting costs of building AI infrastructure and if their lofty future profit expectations are justified. AI isn’t going anywhere, but this valuation dilemma has created a shift from investing in the companies that created AI to those supporting its growth through infrastructure (data centers, energy capacity, etc.) and those starting to benefit most through its utilization (healthcare, financial services, etc.). Time will tell who the ultimate winners are, but these are the times when it pays to be diversified among various sectors and asset classes as market breadth expands.

Important to note, while the Fed has shifted to a hawkish stance, they remain heavily data dependent. The potential resolution to the conflict in the Middle East could send energy prices lower, driving down inflation and re-establishing the Fed’s lower interest rate policy. For now, given the uncertainty, volatility and market leadership shifts, it’s more important than ever to stay diversified and invested for the long-term.

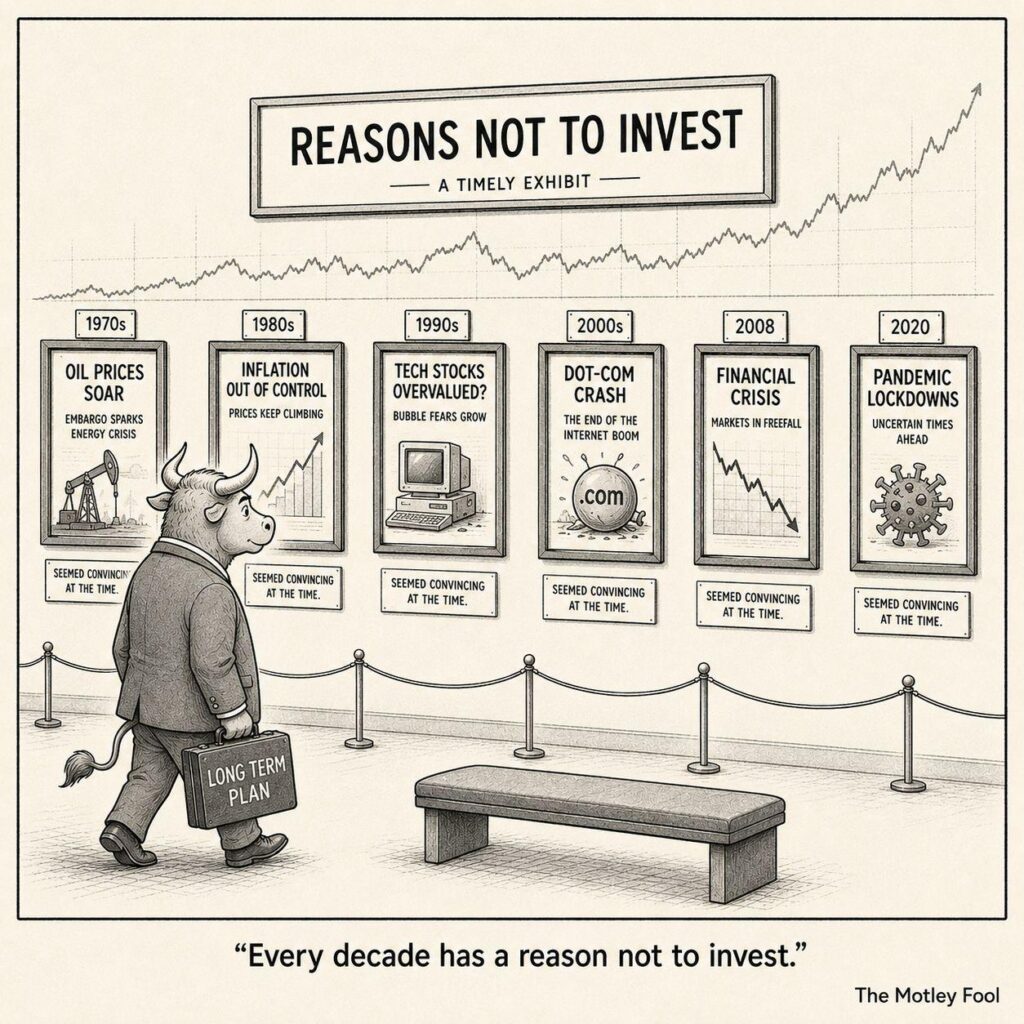

Reasons Not to Invest

A picture is worth a thousand words. I recently ran across the one below from The Motley Fool which shows the various reasons not to invest in the stock market each decade. What’s most interesting is that each of the events has made news headlines this year: from “Oil Prices Soar” to “Hantavirus Fears” and everything in between.

However, there are several great insights hidden in the picture to explore:

- Always Something. At any given time, there is always some reason to not invest in the stock market. Geopolitical… economic… pandemic! And yet the market continues to move up. Separating investing from the headlines is easier said than done, however, taking emotions out of the equation is the key to successfully achieving long-term returns.

- Hindsight 20/20. Below each illustration reads, “Seemed Convincing at the Time.” Everything’s clear in hindsight: “Of course you could have timed when to get out of the market and then get back in!” But no one knows what the market will do or when and what impact certain events may have. We do know, however, that staying invested through the noise often results in a higher probability of positive returns over the long term.

- The Chart Above. You may have missed it, but there is a graph of the S&P 500 above the illustrations. It’s stretched out, so it’s hard to tell what the growth looks like, but I will tell you. If you invested at the start of 1970 through the end of last month, you would have achieved an annualized return of more than 11%. To emphasize what this means, if you invested $10,000 at the start of the period, you would have about $4.3 million today. Always a great reminder about the power of compounding and staying invested for the long term.

Stay diversified, my friends.

Source: The Motley Fool.

As always, Dynamic recommends staying balanced, diversified and invested. Despite short-term market pullbacks, it’s more important than ever to focus on the long-term, improving the chances for investors to reach their goals.

Should you need help navigating client concerns, don’t hesitate to reach out to Dynamic’s Asset Management team at (877) 257-3840, ext. 4 or investmentmanagement@dynamicadvisorsolutions.com.

Disclosures

This commentary is provided for informational and educational purposes only. The information, analysis and opinions expressed herein reflect our judgment and opinions as of the date of writing and are subject to change at any time without notice. This is not intended to be used as a general guide to investing, or as a source of any specific recommendation, and it makes no implied or expressed recommendations concerning the manner in which clients’ accounts should or would be handled, as appropriate strategies depend on the client’s specific objectives.

This commentary is not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. Investors should not assume that investments in any security, asset class, sector, market, or strategy discussed herein will be profitable and no representations are made that clients will be able to achieve a certain level of performance, or avoid loss.

All investments carry a certain risk and there is no assurance that an investment will provide positive performance over any period of time. Information obtained from third party resources are believed to be reliable but not guaranteed as to its accuracy or reliability. These materials do not purport to contain all the relevant information that investors may wish to consider in making investment decisions and is not intended to be a substitute for exercising independent judgment. Any statements regarding future events constitute only subjective views or beliefs, are not guarantees or projections of performance, should not be relied on, are subject to change due to a variety of factors, including fluctuating market conditions, and involve inherent risks and uncertainties, both general and specific, many of which cannot be predicted or quantified and are beyond our control. Future results could differ materially and no assurance is given that these statements or assumptions are now or will prove to be accurate or complete in any way.

Past performance is not a guarantee or a reliable indicator of future results. Investing in the markets is subject to certain risks including market, interest rate, issuer, credit and inflation risk; investments may be worth more or less than the original cost when redeemed.

Investment advisory services are offered through Dynamic Advisor Solutions, LLC, dba Dynamic Wealth Advisors, an SEC registered investment advisor.

Photo: Adobe Stock